埃加奇

EGARCH conditional variance time series model

Description

Use埃加奇指定单变量egarch(指数概括自回归有条件的异质机)模型。这埃加奇function returns an埃加奇对象指定功能形式埃加奇(P,Q) 模型并存储其参数值。

这key components of an埃加奇模型包括:

GARCH polynomial, which is composed of lagged, logged conditional variances. The degree is denoted byP。

Arch多项式,由滞后标准化创新的大小组成。

杠杆作用polynomial, which is composed of lagged standardized innovations.

Maximum of the ARCH and leverage polynomial degrees, denoted byQ。

Pis the maximum nonzero lag in the GARCH polynomial, andQ是拱门中的最大非零滞后,并利用多项式。其他模型组件包括创新平均模型偏移,条件差异模型常数和创新分布。

All coefficients are unknown (NaN值)和可估算的,除非您使用名称值对参数语法指定其值。要估计包含所有或部分未知参数值给定数据的模型,请使用估计。For completely specified models (models in which all parameter values are known), simulate or forecast responses usingsimulate或者预报, respectively.

Creation

Description

MDL= egarch埃加奇目的。

MDL= egarch(P,Q)MDL) with a GARCH polynomial with a degree ofP, 和ARCH and leverage polynomials each with a degree ofQ。All polynomials contain all consecutive lags from 1 through their degrees, and all coefficients areNaNvalues.

This shorthand syntax enables you to create a template in which you specify the polynomial degrees explicitly. The model template is suited for unrestricted parameter estimation, that is, estimation without any parameter equality constraints. However, after you create a model, you can alter property values using dot notation.

MDL= egarch(Name,Value)'Archlags',[1 4],'ARCH',{0.2 0.3}specifies the two ARCH coefficients inARCHat lags1和4。

This longhand syntax enables you to create more flexible models.

Input Arguments

Properties

Object Functions

估计 |

Fit conditional variance model to data |

filter |

Filter disturbances through conditional variance model |

预报 |

预测条件方差模型的条件差异 |

推断 |

Infer conditional variances of conditional variance models |

simulate |

Monte Carlo simulation of conditional variance models |

summarize |

Display estimation results of conditional variance model |

Examples

Create Default EGARCH Model

Create a default埃加奇model object and specify its parameter values using dot notation.

Create an EGARCH(0,0) model.

MDL= egarch

MDL= egarch with properties: Description: "EGARCH(0,0) Conditional Variance Model (Gaussian Distribution)" Distribution: Name = "Gaussian" P: 0 Q: 0 Constant: NaN GARCH: {} ARCH: {} Leverage: {} Offset: 0

MDLis an埃加奇model. It contains an unknown constant, its offset is0, 和the innovation distribution is'Gaussian'。该模型没有GARCH,ARCH或利用多项式。

Specify two unknown ARCH and leverage coefficients for lags one and two using dot notation.

MDL。ARCH = {NaN NaN}; Mdl.Leverage = {NaN NaN}; Mdl

MDL= egarch with properties: Description: "EGARCH(0,2) Conditional Variance Model (Gaussian Distribution)" Distribution: Name = "Gaussian" P: 0 Q: 2 Constant: NaN GARCH: {} ARCH: {NaN NaN} at lags [1 2] Leverage: {NaN NaN} at lags [1 2] Offset: 0

这Q,ARCH, 和杠杆作用特性update to2,{NaN NaN},{NaN NaN}, respectively. The two ARCH and leverage coefficients are associated with lags 1 and 2.

Create EGARCH Model Using Shorthand Syntax

Create an埃加奇model object using the shorthand notation埃加奇(P,Q), wherePis the degree of the GARCH polynomial andQis the degree of the ARCH and leverage polynomial.

创建Egarch(3,2)模型。

mdl = egarch(3,2)

MDL= egarch with properties: Description: "EGARCH(3,2) Conditional Variance Model (Gaussian Distribution)" Distribution: Name = "Gaussian" P: 3 Q: 2 Constant: NaN GARCH: {NaN NaN NaN} at lags [1 2 3] ARCH: {NaN NaN} at lags [1 2] Leverage: {NaN NaN} at lags [1 2] Offset: 0

MDLis an埃加奇模型对象。所有属性MDL, exceptP,Q, 和Distribution, 是NaNvalues. By default, the software:

Includes a conditional variance model constant

不包括条件平均模型偏移(即偏移为

0)在Garch多项式中包括所有滞后术语

PIncludes all lag terms in the ARCH and leverage polynomials up to lag

Q

MDLspecifies only the functional form of an EGARCH model. Because it contains unknown parameter values, you can passMDL和time-series data to估计to estimate the parameters.

Create EGARCH Model Using Longhand Syntax

Create an埃加奇model object using name-value pair arguments.

Specify an EGARCH(1,1) model. By default, the conditional mean model offset is zero. Specify that the offset isNaN。Include a leverage term.

MDL= egarch('GARCHLags',1,'Archlags',1,'LeverageLags',1,'抵消',Nan)

MDL= egarch with properties: Description: "EGARCH(1,1) Conditional Variance Model with Offset (Gaussian Distribution)" Distribution: Name = "Gaussian" P: 1 Q: 1 Constant: NaN GARCH: {NaN} at lag [1] ARCH: {NaN} at lag [1] Leverage: {NaN} at lag [1] Offset: NaN

MDLis an埃加奇模型对象。这software sets all parameters toNaN, exceptP,Q, 和Distribution。

SinceMDLcontainsNaNvalues,MDLis appropriate for estimation only. PassMDL和time-series data to估计。

Create EGARCH Model with Known Coefficients

创建具有平均偏移量的Egarch(1,1)模型

在哪里

和 is an independent and identically distributed standard Gaussian process.

MDL= egarch('持续的',0.0001,'GARCH',0.75,。。。'ARCH',0.1,'抵消',0.5,'Leverage',{-0.3 0 0.01})

mdl =带有属性的egarch:描述:“ egarch(1,3)条件方差模型具有偏移(高斯分布)”分布:name =“ gaussian” p:1 q:3常数:0.0001 garch:{0.75}在lag [1]] Arch:{0.1}在滞后[1]杠杆:{-0.3 0.01} lags [1 3]偏移:0.5

埃加奇assigns default values to any properties you do not specify with name-value pair arguments. An alternative way to specify the leverage component is'Leverage',{-0.3 0.01},'LeverageLags',[1 3]。

Access EGARCH Model Properties

Access the properties of a created埃加奇使用点表示法模型对象。

Create an埃加奇模型对象。

mdl = egarch(3,2)

MDL= egarch with properties: Description: "EGARCH(3,2) Conditional Variance Model (Gaussian Distribution)" Distribution: Name = "Gaussian" P: 3 Q: 2 Constant: NaN GARCH: {NaN NaN NaN} at lags [1 2 3] ARCH: {NaN NaN} at lags [1 2] Leverage: {NaN NaN} at lags [1 2] Offset: 0

从模型中删除第二个GARCH术语。也就是说,指定第二滞后条件差异的GARCH系数是0。

MDL。garch {2} = 0

MDL= egarch with properties: Description: "EGARCH(3,2) Conditional Variance Model (Gaussian Distribution)" Distribution: Name = "Gaussian" P: 3 Q: 2 Constant: NaN GARCH: {NaN NaN} at lags [1 3] ARCH: {NaN NaN} at lags [1 2] Leverage: {NaN NaN} at lags [1 2] Offset: 0

这GARCH polynomial has two unknown parameters corresponding to lags 1 and 3.

Display the distribution of the disturbances.

MDL。Distribution

ans =struct with fields:Name: "Gaussian"

这disturbances are Gaussian with mean 0 and variance 1.

Specify that the underlying disturbances have atdistribution with five degrees of freedom.

MDL。Distribution = struct('Name','t','DoF',5)

MDL= egarch with properties: Description: "EGARCH(3,2) Conditional Variance Model (t Distribution)" Distribution: Name = "t", DoF = 5 P: 3 Q: 2 Constant: NaN GARCH: {NaN NaN} at lags [1 3] ARCH: {NaN NaN} at lags [1 2] Leverage: {NaN NaN} at lags [1 2] Offset: 0

Specify that the ARCH coefficients are 0.2 for the first lag and 0.1 for the second lag.

MDL。ARCH = {0.2 0.1}

MDL= egarch with properties: Description: "EGARCH(3,2) Conditional Variance Model (t Distribution)" Distribution: Name = "t", DoF = 5 P: 3 Q: 2 Constant: NaN GARCH: {NaN NaN} at lags [1 3] ARCH: {0.2 0.1} at lags [1 2] Leverage: {NaN NaN} at lags [1 2] Offset: 0

To estimate the remaining parameters, you can passMDL和your data to estimate and use the specified parameters as equality constraints. Or, you can specify the rest of the parameter values, and then simulate or forecast conditional variances from the GARCH model by passing the fully specified model tosimulate或者预报, respectively.

Estimate EGARCH Model

Fit an EGARCH model to an annual time series of Danish nominal stock returns from 1922-1999.

Load theData_Danishdata set. Plot the nominal returns (RN).

loadData_Danish;nr = DataTable.RN; figure; plot(dates,nr); hold在;plot([dates(1) dates(end)],[0 0],'r:');% Plot y = 0holdoff;标题(“丹麦名义股票返回”);ylabel('Nominal return (%)');xlabel(“年”);

这nominal return series seems to have a nonzero conditional mean offset and seems to exhibit volatility clustering. That is, the variability is smaller for earlier years than it is for later years. For this example, assume that an EGARCH(1,1) model is appropriate for this series.

Create an EGARCH(1,1) model. The conditional mean offset is zero by default. To estimate the offset, specify that it isNaN。Include a leverage lag.

MDL= egarch('GARCHLags',1,'Archlags',1,'LeverageLags',1,'抵消',Nan);

Fit the EGARCH(1,1) model to the data.

estmdl= estimate(Mdl,nr);

埃加奇(1,1) Conditional Variance Model with Offset (Gaussian Distribution): Value StandardError TStatistic PValue _________ _____________ __________ _________ Constant -0.62723 0.74401 -0.84304 0.3992 GARCH{1} 0.77419 0.23628 3.2766 0.0010508 ARCH{1} 0.38636 0.37361 1.0341 0.30107 Leverage{1} -0.002499 0.19222 -0.013001 0.98963 Offset 0.10325 0.037727 2.7368 0.0062047

estmdl是完全指定的埃加奇模型对象。也就是说,它不包含NaNvalues. You can assess the adequacy of the model by generating residuals using推断, 和then analyzing them.

To simulate conditional variances or responses, passestmdltosimulate。

To forecast innovations, passestmdlto预报。

Simulate EGARCH Model Observations and Conditional Variances

模拟完全指定的条件差异或响应路径埃加奇模型对象。That is, simulate from an estimated埃加奇model or a known埃加奇model in which you specify all parameter values.

Load theData_Danishdata set.

loadData_Danish;rn = DataTable.RN;

Create an EGARCH(1,1) model with an unknown conditional mean offset. Fit the model to the annual, nominal return series. Include a leverage term.

MDL= egarch('GARCHLags',1,'Archlags',1,'LeverageLags',1,'抵消',Nan);estmdl= estimate(Mdl,rn);

埃加奇(1,1) Conditional Variance Model with Offset (Gaussian Distribution): Value StandardError TStatistic PValue _________ _____________ __________ _________ Constant -0.62723 0.74401 -0.84304 0.3992 GARCH{1} 0.77419 0.23628 3.2766 0.0010508 ARCH{1} 0.38636 0.37361 1.0341 0.30107 Leverage{1} -0.002499 0.19222 -0.013001 0.98963 Offset 0.10325 0.037727 2.7368 0.0062047

模拟100路径的条件方差和再保险sponses from the estimated EGARCH model.

numObs = numel(rn);% Sample size (T)numPaths = 100;% Number of paths to simulaterng(1);% For reproducibility[VSim,YSim] = simulate(EstMdl,numObs,“数字”,numPaths);

VSim和YSIM是T-by-numPaths矩阵。行对应于样本周期,列对应于模拟路径。

Plot the average and the 97.5% and 2.5% percentiles of the simulate paths. Compare the simulation statistics to the original data.

VSimBar = mean(VSim,2); VSimCI = quantile(VSim,[0.025 0.975],2); YSimBar = mean(YSim,2); YSimCI = quantile(YSim,[0.025 0.975],2); figure; subplot(2,1,1); h1 = plot(dates,VSim,'Color',0.8*ones(1,3)); hold在;h2 = plot(dates,VSimBar,'k--','LineWidth',2);h3 =图(日期,vsimci,'r--','LineWidth',2);holdoff;标题('Simulated Conditional Variances');ylabel('Cond. var.');xlabel(“年”);subplot(2,1,2); h1 = plot(dates,YSim,'Color',0.8*ones(1,3)); hold在;h2 = plot(dates,YSimBar,'k--','LineWidth',2);h3 = plot(dates,YSimCI,'r--','LineWidth',2);holdoff;标题('Simulated Nominal Returns');ylabel('Nominal return (%)');xlabel(“年”);legend([h1(1) h2 h3(1)],{'Simulated path''Mean''Confidence bounds'},。。。'FontSize'7'地点','西北');

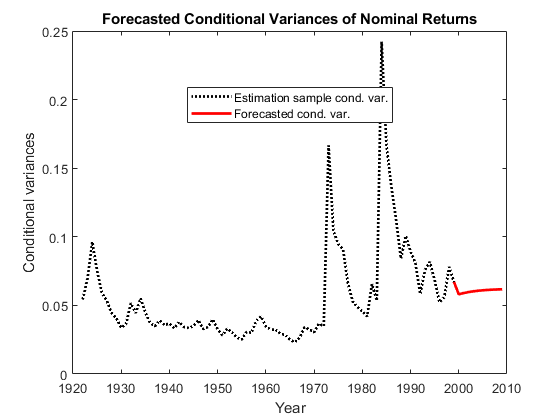

Forecast EGARCH Model Conditional Variances

Forecast conditional variances from a fully specified埃加奇模型对象。That is, forecast from an estimated埃加奇model or a known埃加奇model in which you specify all parameter values. The example follows fromEstimate EGARCH Model。

Load theData_Danishdata set.

loadData_Danish;nr = DataTable.RN;

Create an EGARCH(1,1) model with an unknown conditional mean offset and include a leverage term. Fit the model to the annual nominal return series.

MDL= egarch('GARCHLags',1,'Archlags',1,'LeverageLags',1,'抵消',Nan);estmdl= estimate(Mdl,nr);

埃加奇(1,1) Conditional Variance Model with Offset (Gaussian Distribution): Value StandardError TStatistic PValue __________ _____________ __________ _________ Constant -0.62723 0.74401 -0.84304 0.39921 GARCH{1} 0.77419 0.23628 3.2766 0.0010507 ARCH{1} 0.38636 0.37361 1.0341 0.30107 Leverage{1} -0.0024989 0.19222 -0.013 0.98963 Offset 0.10325 0.037727 2.7368 0.0062047

预测使用估计的Egarch模型将未来10年的名义返回序列的条件差异。将整个返回序列指定为前样品观测值。该软件使用预先样本观测和模型进一步进一步的条件差异。

numPeriods = 10; vF = forecast(EstMdl,numPeriods,nr);

Plot the forecasted conditional variances of the nominal returns. Compare the forecasts to the observed conditional variances.

v = infer(EstMdl,nr); figure; plot(dates,v,'k:','LineWidth',2);hold在;plot(dates(end):dates(end) + 10,[v(end);vF],'r','LineWidth',2);标题('Forecasted Conditional Variances of Nominal Returns');ylabel('Conditional variances');xlabel(“年”);legend({'Estimation sample cond. var.','Forecasted cond. var.'},。。。'地点','Best');

More About

Tips

You can specify an

埃加奇model as part of a composition of conditional mean and variance models. For details, seearima。一个EGARCH(1,1)规范是足够复杂most applications. Typically in these models, the GARCH and ARCH coefficients are positive, and the leverage coefficients are negative. If you get these signs, then large unanticipated downward shocks increase the variance. If you get signs opposite to those signs that are expected, you can encounter difficulties inferring volatility sequences and forecasting. A negative ARCH coefficient is problematic. In this case, an EGARCH model might not be the best choice for your application.

References

[1] Tsay, R. S.Analysis of Financial Time Series。3rd ed. Hoboken, NJ: John Wiley & Sons, Inc., 2010.

See Also

Objects

Topics

- Specify EGARCH Models

- Modify Properties of Conditional Variance Models

- 指定条件均值和方差模型

- Infer Conditional Variances and Residuals

- Compare Conditional Variance Models Using Information Criteria

- Assess EGARCH Forecast Bias Using Simulations

- Forecast a Conditional Variance Model

- Conditional Variance Models

- EGARCH Model

Select a Web Site

Choose a web site to get translated content where available and see local events and offers. Based on your location, we recommend that you select:。

Selectweb siteYou can also select a web site from the following list:

Americas

- América Latina(Español)

- Canada(English)

- United States(English)

欧洲

- Netherlands(English)

- 挪威(English)

- Österreich(德意志)

- Portugal(English)

- 瑞典(English)

- Switzerland

- United Kingdom(English)